News

Blog

My Blog…

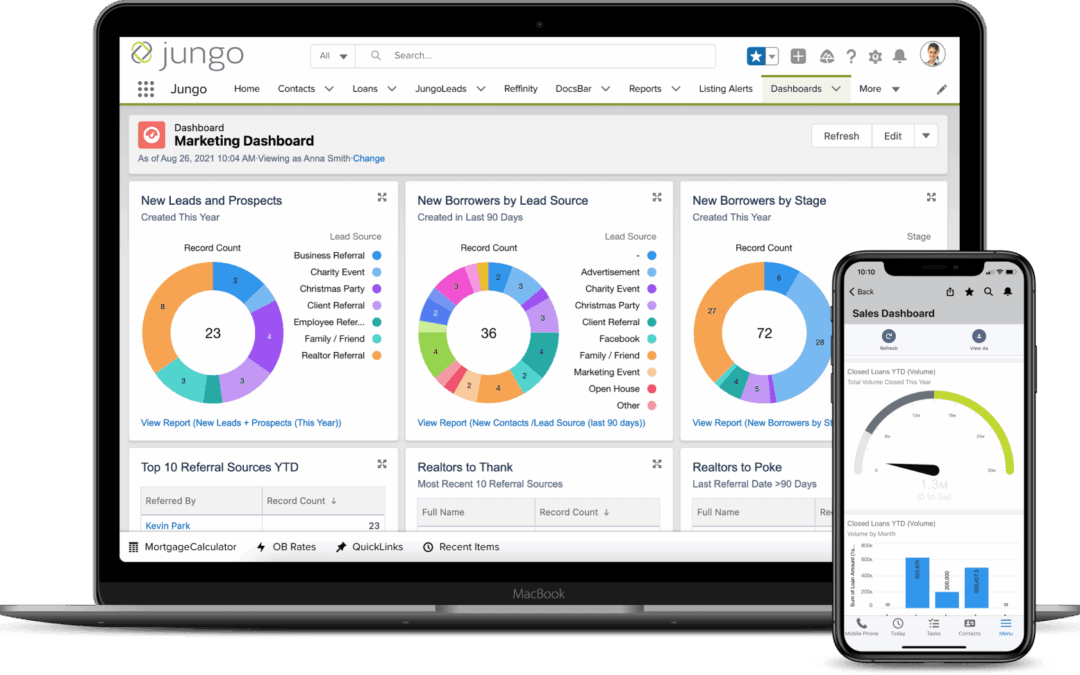

A Mortgage CRM

Here is a simplified, roadmap-style summary of how to build a Mortgage CRM.

The Core Concept

A generic CRM (like Salesforce) manages sales. A Mortgage CRM manages the loan lifecycle. It must handle strict financial compliance, integrate with banking systems, and track a loan from “Lead” to “Funded.”

Phase 1: The Core Features (MVP)

The system needs to manage two main things: People and the Process.

-

Lead Intake: Automatically grab leads from websites (like Zillow) and create a profile.

-

The Loan Pipeline (Kanban Board): A visual dashboard moving the loan through stages:

-

New Lead → Application → Processing → Underwriting → Clear to Close → Funded.

-

-

Automation:

-

Updates: When a loan moves to “Underwriting,” the system automatically emails the borrower and realtor.

-

Marketing: Automatic birthday wishes or “Rate Drop” alerts to past clients.

-

-

Document Portal: A secure login for borrowers to upload sensitive docs (tax returns, pay stubs) safely.

Phase 2: The Data Structure

Mortgage data is relational. Your database needs to link these four entities:

-

Users: Your internal team (Loan Officers, Processors, Admins).

-

Contacts: External people (Borrowers, Co-borrowers, Realtors).

-

The Loan: The financial deal (Amount, Interest Rate, Property Address, Status).

-

Activities: History of calls, emails, and notes tied to that loan.

Phase 3: Recommended Tech Stack

Security and data structure are more important here than in a standard app.

-

Frontend (The Look): React or Next.js. Best for building complex dashboards and drag-and-drop pipelines.

-

Backend (The Logic): Node.js (good for real-time notifications) or Python (better if you plan to add AI for calculating rates later).

-

Database (The Storage): PostgreSQL. You need a structured, SQL database for financial data.

-

Storage: AWS S3 with encryption enabled for storing borrower documents.

Phase 4: Critical Integrations

Your CRM cannot live in a bubble. It must communicate with the mortgage ecosystem via APIs:

-

Loan Origination System (LOS): The software banks use to actually underwrite the loan (e.g., Encompass, Calyx).

-

Pricing Engines: Tools like Optimal Blue to fetch live interest rates.

-

Communication: Twilio or SendGrid for sending automated texts and emails.

Phase 5: Security & Compliance (Non-Negotiable)

Because you are handling “Personally Identifiable Information” (PII) like Social Security Numbers, security is the top priority.

-

Encryption: Data must be scrambled (encrypted) when stored in the database and when moving over the internet.

-

Audit Logs: You must track who looked at a file and when.

-

Permissions (RBAC): A “Junior Loan Officer” should only see their own clients, whereas a “Manager” can see everything.

Next Steps

-

Mockups: Sketch the dashboard. How does a Loan Officer view their pipeline?

-

The “Hook”: Why would a lender buy this? Usually, the answer is “It automates the updates that Loan Officers forget to send.”

-

Build vs. Buy: Are you building a SaaS product to sell to many lenders, or a custom tool for just one?

Building a Mortgage CRM

News